YOUR HOME SOLD GUARANTEED OR WE'LL BUY IT!*

July 2024 Calgary Real Estate: Inventory Growth and Its Effects on Home Prices

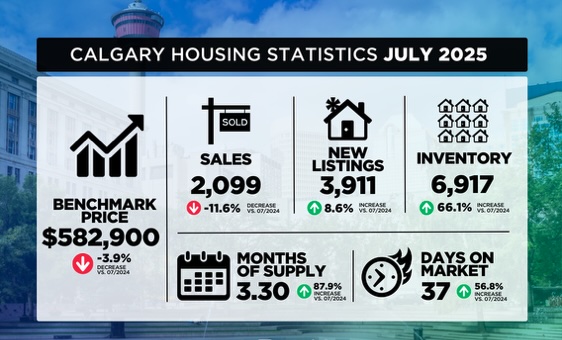

In July, inventory levels across Calgary experienced a notable increase, reaching 6,917 units, the highest recorded since before the pandemic. This surge in supply was particularly prominent in areas that have seen new community development, contributing to a greater variety of housing options. While the overall market saw improvements in supply across all property types and districts, the largest changes were observed in the newer suburban communities, where additional housing has helped stabilize availability.

However, the growing supply has led to downward pressure on home prices in certain parts of the city. Calgary's residential benchmark price has been declining gradually over the last few months, dropping by 4% from its peak in June 2024. Despite this dip, the price reduction is not uniform across all types of homes or areas. While some sectors of the market, like apartments and row-style homes in the North East and North districts, have seen steeper declines, these price drops have not completely undone the gains achieved in recent years.

The slowdown in sales activity further compounded the effects of rising inventory. In July, sales fell by 12% compared to last year, while new listings rose by over 8%, signaling a shift towards a more balanced market. The competition from newly built homes, along with slower sales and a lack of rate cuts by the central bank, contributed to the cooling of the market. Apartments, in particular, faced higher inventory levels, with the months of supply surpassing four months, while detached and semi-detached homes maintained more balanced conditions with around three months of supply.

Detached homes saw a slight uptick in the months of supply, rising to three months for the first time since 2020. Although sales activity slowed to 1,031 units in July, new listings remained robust, resulting in more inventory and a shift towards a balanced market. Notably, price adjustments varied by district, with the North East and East areas experiencing larger price declines of about 5%, while the City Centre saw a modest price increase of nearly 2%. These regional differences reflect how local market conditions can significantly affect overall trends.

In the semi-detached and row home segments, price stability was the overarching trend despite the increase in supply. Semi-detached homes saw a 1% increase in benchmark prices compared to last year, with some districts, such as the City Centre, witnessing higher gains. Row homes, however, experienced a slight decline in price, down by about 4% compared to the previous year. In terms of supply, both property types showed a rise in the months of supply, pushing the market closer to equilibrium, especially in areas with higher inventory levels, such as the North East and North districts.